Storage chips are skyrocketing again, what's going on?

Recently, there have been constant updates on storage chips. According to media reports, Samsung Electronics has taken the lead in suspending the October DDR5 DRAM contract quotation, triggering other storage manufacturers such as SK Hynix and Micron to follow suit. On November 14th, according to industry insiders, Samsung has resumed quoting DDR5 contracts. After restoring the quotation, the contract price for Samsung's 32GB DDR5 memory chip module in November increased from $149 in September to $239, a 60% increase in price.

1. storage chip, skyrocketing in all aspects

If there is one word to describe the current storage chip market, it would be: crazy.

What has the current storage chip grown to?

At present, although there have been continuous news of price increases for both DRAM and NAND Flash, the increase and attention to DRAM are higher.

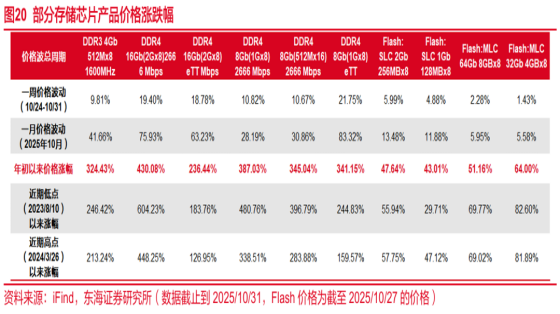

Looking at the big data first, according to a report from Donghai Securities, the regular 16Gb DDR4 in October increased by 75.93% compared to the previous month, the regular 8Gb DDR4 increased by about 30%, and the 4Gb DDR3 increased by 41.66%. The report shows that the overall prices of DRAM and NAND Flash continued to rise in October, and the increase continued to expand month on month. It is expected that the prices of storage chips will continue to rise in November 2025.

After entering November, according to the latest data from TrendForce, the price of mainstream DDR4 1Gx8 3200MT/s chips increased by 7.10% from $11.071 to $11.857 during the week of November 5th to 11th. The pricing of particles (in Gb units) has already surpassed the pricing of modules with the same capacity, and the price difference is huge.

Unlike before, DDR5 prices have also skyrocketed this time, with Caixin reporting that spot prices for DDR5 have surged by 25% within a week. Morgan Stanley also reported in November that spot prices for DDR5 (16Gb) have skyrocketed from $7.5 in September to $20.9, and stated that "DRAM prices have surpassed historical highs".

In terms of spot market, DDR4 chips are still the most popular, with both 8GB and 16GB being very hot and showing significant growth.

Samsung's 8G DDR4 chip K4A8G165WC-BCTD, which was still priced at $1.7 in March this year, skyrocketed to around $7.5 in June, rebounded to just over $7 in August, and was priced at around $8 at the end of October. It has now been quoted for $13.

The distributor specializing in Micron stated that the price of Micron 8G DDR4 was between $1.15-1.25 in November and December last year, gradually rising to $3 in May, skyrocketing to $8+after the news of discontinuation in June, and then dropping back to around $7 in August. Currently, the price is between $13-15, with industrial grade prices slightly higher than commercial grade prices.

Micron's 16GB DDR4 increased from $2.88 in November December last year to over $5.5 in May, and the transaction price rose to $20-21 in June. In early September, the price of 16GB industrial grade DDR4 was around $21, and after the price increase news, it rose by about 30%. Commercial grade DDR4 will be relatively cheaper.

Now, the commercial grade transaction price of Micron's 16GB DDR4 has skyrocketed to around $60, while the industrial grade quotation has reached as high as $100.

In addition to DDR4, the prices of DDR3 and DDR5 have also significantly increased.

The DDR3 chip K4B4G1646E-BYMA of Samsung 4G, which was priced at $2 at the end of October, has now risen to $3.5.

However, there are not many products circulating in the DDR5 market, and some chip distributors have stated that "DDR5 manufacturers do not accept orders or ship". Therefore, most distributors are aware that DDR5 has also skyrocketed, but they are not very familiar with the specific models and price increases.

A chip distributor shared the price changes of some DDR5 models, with prices doubling in the past week. Some distributors have also stated that their commonly used Micron 8Gb LPDDR5X chip, which was priced at $25 in July, has now risen to $50.

In addition, there are also news of price increases for LPDDR4 and LPDDR5.

The price increase of storage chips has not just started now. Let's briefly review the market changes of storage chips since the beginning of this year:

In February and March of this year, due to the news of Samsung's MLC discontinuation in October last year, small capacity eMMCs using MLC NAND began to increase in price;

At the same time, in February, it was reported that the three major manufacturers would cease production of DDR4. Starting from February and March, DDR4 chips also began to increase in price. By April and May, some DDR4 prices had doubled compared to March, with Samsung experiencing the highest increase. Since then, the trend of DDR4 chip price increases has continued, becoming the most eye-catching product in the storage spot market;

In mid June, Micron's announcement of the discontinuation of DDR4 ignited the market, and some suppliers began to hold back on their sales. DDR4 prices doubled again on the basis of the original price increase. Previously, Micron's DDR4, which had not increased much, rose by 150% -400%. Micron's LPDDR4, DDR3, and LPDDR5 also saw a significant increase;

In August, the market calmed down a bit, and DDR4 as a whole entered a high-level sideways phase. Most models stopped skyrocketing and prices tended to stabilize, while some part numbers experienced price corrections;

On September 12th, media reported that Micron's storage products such as DDR4, DDR5, LPDDR4, and LPDDR5 will soon increase by 20% -30%. On September 18th, media reported that Samsung notified major customers that the prices of DRAM LPDDR4X and LPDDR5/5X protocols are expected to increase by more than 15% -30% in the fourth quarter, and the production capacity of DDR4 related products is expected to be only 20% of that in 2025 in 2026. On September 23rd, TrendForce reported that SK Hynix is reportedly negotiating price adjustments with customers based on market conditions.

In early October, OpenAI announced strategic partnerships with Samsung Electronics and SK Hynix, two Korean storage chip giants, to supply advanced storage chips to the Stargate project. After the National Day holiday, the storage spot market experienced a comprehensive surge.

On November 3rd, media reported that Samsung Electronics had temporarily suspended its DDR5 DRAM contract quotes for October, prompting other storage manufacturers such as SK Hynix and Micron to follow suit. The resumption of quotes is expected to be postponed until mid November. TrendForce points out that the current quotation cycle has shifted from the original "quarterly" framework to a "monthly" quotation.

The storage chip market has completely gone crazy.

On November 17th, Reuters reported that according to industry insiders, Samsung has resumed quoting DDR5 contracts. After restoring the quotation, the contract price for Samsung's 32GB DDR5 memory chip module in November increased from $149 in September to $239, a 60% increase in price.

The storage market may usher in new changes again.

2.Why is it skyrocketing again?

Overall, since February and March of this year, storage chips have started to increase in price. Initially, it was small capacity eMMC, followed by DDR4 leading the continuous rise. In mid June, the market was ignited by Micron's announcement of production stoppage, and DDR4 entered a high-level sideways phase in July and August. Based on previous analysis, the main reasons for the previous surge in storage were: the shutdown, production conversion, and price increase news of the three major storage companies, Micron's recognition of the shutdown information, tariffs, and external environmental changes.

The recent surge, in addition to previous factors, may be mainly due to the outbreak of AI demand in North America, the backlog of production capacity, the suspension of contract quotes by original factories, the amplification of real demand under the sentiment of price increases, and the frequent release of various positive news, which generally favors the demand after storage.

On the original factory side, in addition to suspending contract quotations, Securities Times reported that in the fourth quarter, upstream original factories only provided quotations to technology leaders or first tier cloud vendors, and DDR5 almost did not release production capacity to other general customers. Storage has "fully entered the seller's market". In addition, the supply strategy of the three major original storage factories will become increasingly strict in the future, only providing quotes to long-term customers. This also means that not providing quotes from the original factory may become the norm, forcing customers with urgent needs to turn to the spot market to grab goods.

According to Securities Times, industry insiders have revealed that although the rise in storage contract prices for the fourth quarter has become a market consensus, the previous expectation was that the fourth quarter contract prices could be finalized before the end of October. But Samsung was reluctant to provide a contract quote and directly told downstream customers that there was "no stock to sell", resulting in a 25% surge in spot prices for DDR5 in just one week.

Now, institutions generally see this round of price increases as the start of a storage "super cycle", and the core driving force is AI. The production capacity of the three major DRAM companies has been locked in advance by top customers such as OpenAI, Amazon, Google, etc. Taking OpenAI's "Stargate" as an example, the project requires 900000 DRAM wafers per month. Goldman Sachs analyzed that this number is approximately equivalent to 57% of the current combined production capacity of Samsung Electronics, SK Hynix, and Micron.

The three major manufacturers are prioritizing the investment of advanced production capacity in high-end server DRAM and HBM, which limits the supply of PC, mobile, and consumer markets, and significantly reduces the supply of consumer and small and medium-sized customers. Driven by strong orders related to servers, SK Hynix's latest quarterly revenue increased by 39.3% year-on-year, Micron increased by 46% year-on-year, and Samsung increased by 8.84% year-on-year.

In the spot market, under the influence of price increases, demand signals are often amplified, causing the original real demand to be exaggerated several times and further raising prices.

According to TrendForce data, as of the end of the third quarter of 2025, global DRAM inventory turnover was only 3.3 weeks, reaching a low level in 2018. In addition, some chip distributors have revealed that the price of ordering from the original factory has doubled and the delivery time is also very long, all of which have further pushed up the spot price.

In addition, various institutions have frequently released positive news recently, such as confirming the doubling of storage prices, raising target stock prices for storage related manufacturers, predicting this cycle, pointing out huge supply and demand gaps, and so on. Under the combination of various factors, the market becomes even more 'crazy'.

3.Conclusion

The current storage spot market is indeed crazy, and prices have indeed skyrocketed. But what about the real demand for storage?

The flash memory market has reported a sharp rise in the spot market for DDR4 chips, with some prices inverted with DDR5 of the same capacity. It is evident that consumer customers find it difficult to accept such high cost DDR4 products. The storage agent interviewed by Interface News stated that the actual demand for channels has not increased significantly and is similar to previous years, at most remaining the same. The real reason is not that demand has improved, but that there is a shortage of goods upstream.

Some chip distributors have stated that the current transaction targets are mostly traders, and some end customers are looking for old batches of materials. However, some external orders cannot accept old batches and are still being transacted even at high prices.

What do you think of this storage market trend?

Related Information

- 1500+ Daily average RFQ Volume

- 20,000.000 Standard Product Unit

- 1800+ Worldwide Manufacturers

- 15,000+ In-stock Warehouse